Not everyone has paid employment with group health insurance. The Affordable Healthcare Act (ACA) tries to solve this challenge with its comprehensive marketplace where people can find insurance plans for individuals and small businesses. In this market, you’ll find various companies selling competitive insurance products. So, you can choose government-regulated and affordable healthcare plans from participating insurers within the marketplace.

How does the ACA Health Insurance Marketplace work, and what are its benefits? We explain everything you need to know in this article.

- What Is the ACA Health Insurance Marketplace?

- How Does It Work?

- What Types of Health Plans Are Available?

- Who Is Eligible for ACA Health Insurance?

- How To Enroll in a Marketplace Plan

- What Is the Processing Time?

- What Should You Do If Your Application Is Denied?

- How Does the ACA Marketplace Connect With Medicaid and CHIP?

- Helping Uninsured Americans Get Health Coverage

What Is the ACA Health Insurance Marketplace?

Created and signed into law by the President Obama administration in 2010, this healthcare reform initiative has created an open health marketplace or health exchange where individuals and small businesses can find standardized healthcare plans.

Whether you know it as Obamacare or the Patient Protection and Affordable Care Act (PPACA), the Affordable Care Act (ACA) has only one goal: to help uninsured Americans access subsidized health insurance packages from private insurance providers.

How Does It Work?

The ACA Marketplace program is a government initiative run by the Center for Medicare and Medicaid Services (CMS), a unit under the Department of Health and Human Services (DHHS). However, they are operated within individual states.

The role of the marketplace is to create a competitive environment where people can assess different insurance companies before opting for a coverage option. Though each provider has unique offerings, the mandatory benefits they must offer include:

- Emergency services

- Hospitalization

- Laboratory services

- Ambulatory patient services

- Pediatric services

- Mental health-related services

- Pregnancy, maternity and newborn care

- Prescription medications

- Rehabilitative and habilitative services

- Chronic disease management and preventive and wellness services

What Types of Health Plans Are Available?

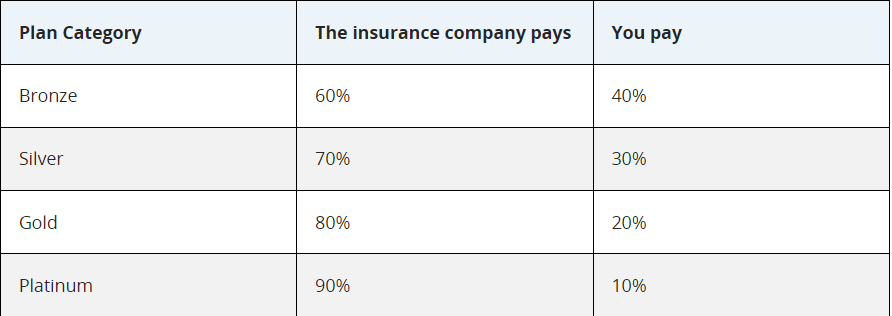

The ACA Health Marketplace offers a four-tiered plan, with bronze having the lowest monthly premium and platinum having the highest. There are also catastrophic health plans with lower monthly premiums, but you must pay routine medical bills out of pocket.

These are the same health plans for Obamacare 2024, but we highlight the cost-sharing structure for each plan in the image below:

To compare Marketplace plans, visit the HealtCare.gov plan comparison website, enter your zip code to find a marketplace near you, and see the final prices before enrolling. For instance, if you live in California’s Nevada County, your state’s Marketplace is Covered California.

Typically, the benefits last a year. Your plan will automatically renew if you don’t cancel it, and your insurance company will send a notice of your renewal status when a renewal is initiated. However, comparing different plans annually can help you find the best offers.

Who Is Eligible for ACA Health Insurance?

One of the perks of the ACA Health Insurance Marketplace is that it requires no income limit. However, you must qualify for the program before enrolling in a plan. To be eligible, you must meet the requirements below:

- Be a legal US resident

- Be a US citizen or an eligible immigrant (undocumented people cannot get help through the ACA Marketplace)

- Must not be in prison, jail, or be incarcerated

Is Your Healthcare Provider on the Marketplace?

The easiest way to find out if your current healthcare provider offers a marketplace plan is to check HealtCare.gov or your local Marketplace website. You can also make direct enquiries from the provider or the insurance company you want to get a plan from.

How To Qualify for Subsidies and Financial Assistance

You can get financial assistance from ACA Marketplaces through premium tax credit (PTC) and cost-sharing reduction (CSR) for low- and middle-income earners who purchase any of the program’s coverage. However, there are eligibility requirements, including:

- Being a US citizen or a legal immigrant

- Having annual earnings within 100% and 400% of the FPL

- Getting a coverage plan from the Marketplace

How To Enroll in a Marketplace Plan

Since there are numerous plans to choose from, getting a Marketplace plan begins with finding a Marketplace with enrollment options within your state. To do this, visit the HealthCare.gov website to find a local Health Insurance Marketplace. You can choose a plan for the first time or make changes to an existing plan.

Besides the eligibility requirements above, other documents you’ll need to enroll include:

- A birth certificate or proof of identity

- Evidence of income, such as pay stubs or a W-2 Form

- Proof of citizenship or legal immigration status

- Dependent information, if applicable

You can also apply over the phone or physically at an enrollment assistance center. However, to qualify, you must hand in your application when enrollment is open. You can find more details about the open enrollment schedule and deadlines here.

Making Changes to Enrollment

You can modify your plan when the enrollment window is open. For instance, you may switch from one plan tier to another, include new dependents, and update your income information. Your coverage annual renewal is also expected to happen during open enrollment. However, you may qualify for special enrollment to change your plan or other details outside the open enrollment period.

It’s important to note that you must have experienced a qualifying life event like giving birth to a new child, relocating outside your current city or county, or experiencing a change in income. You must also be able to prove these events with supporting documents.

What Is the Processing Time?

Typically, a Marketplace application takes about 30 minutes to complete. However, the website experiences excessive traffic from applicants when enrollments are open. Once you choose a plan, it’ll take a few more minutes to enroll.

What Should You Do If Your Application Is Denied?

Cross-check the information provided to correct errors. If you think a mistake has been made, you can appeal the decision through your account or by speaking with an ACA-registered agent.

Interestingly, there are Marketplace Navigators and Counselors to provide free guidance. You can find them using the “ Find Local Help” section on HealthCare.gov.

How Does the ACA Marketplace Connect With Medicaid and CHIP?

The ACA, Medicaid, and the Children’s Health Insurance Program (CHIP) connect in different ways. All of them offer health insurance coverage to individuals and families, and you can enroll in CHIP and Medicaid through the ACA Marketplace. However, if you are currently receiving Medicaid benefits, you are not eligible for ACA Marketplace plans.

Helping Uninsured Americans Get Health Coverage

If you lose Medicaid or CHIP or do not qualify for the programs, a great way to keep you and your family covered is through the Affordable Care Act (ACA) Health Insurance Marketplace. From ACA-compliant health insurance for international students to other plans for families, the exchange provides you with subsidized care plans from various insurance companies.

You can call 1-800-318-2596 (TTY: 1-855-889-4325) to apply for an ACA Marketplace plan on the phone, appeal a decision, or get help.