Every month, approximately 6 million individuals either lose or leave their jobs, often raising concerns about the continuity of their group health insurance. The Consolidated Omnibus Budget Reconciliation Act (COBRA) offers a solution, allowing you to temporarily retain your employer-sponsored health plan even after job loss or resignation. However, COBRA coverage isn’t automatically granted. Before you apply, it’s crucial to understand the eligibility requirements and application process. This article will guide you through everything you need to know about COBRA and how to secure this vital benefit.

What Is COBRA Insurance?

The Consolidated Omnibus Budget Reconciliation Act (COBRA) is an initiative that allows qualified US workers and their families to enjoy health insurance from their employers after losing their jobs or for other acceptable reasons. Its goal is to give qualified individuals and their loved ones temporary medical support.

How Does It Work?

COBRA is a channel for you and your dependents to continue getting similar group health benefits as those in your employment contract legally. With this program, it doesn’t matter whether you quit the job, got fired, or had your working hours reduced.

The US Department of Labor (DOL) is in charge of the initiative. The agency states that companies with at least 20 employees must offer their staff health benefits, so long as the staff members are willing to pay the bills on their own.

More often than not, you’ll be required to cover 100% of the total insurance costs and an additional 2% administrative fee to stay on the group health plan. The plan includes:

- Impatient and outpatient hospital care

- Prescription drugs

- Surgery and major medical occurrences

- Physician care

- Dental and vision care

Usually, your employer will notify you and your family members are eligible for COBRA after you meet the qualifying conditions. However, you can confirm this from the company’s Human Resources department or employee handbook.

Who Is Eligible for COBRA Insurance?

An employer with 20 team members or more is expected to support COBRA, but you won’t qualify for the benefits just by being an employee. Here are the requirements when thinking of how to get COBRA insurance:

- You have a group health plan at work that is covered by COBRA

- A qualifying event happens, and you are a beneficiary

- You are a family member or dependent (a spouse or child) to the qualified beneficiary

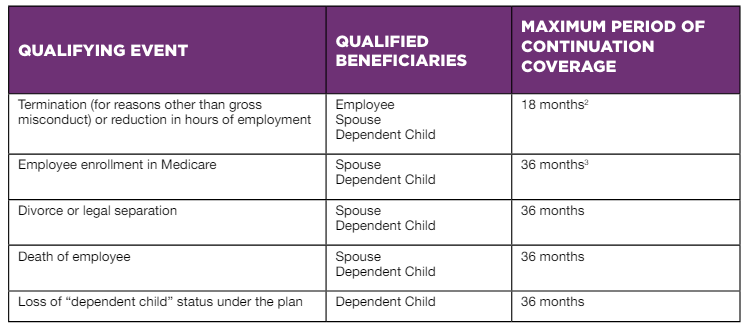

COBRA’s qualifying events are those that can make you lose your group health coverage. These include:

- The individual or company terminating an employment contract for reasons besides gross misconduct.

- A reduction of the employee’s working hours

- The covered individual is entitled to Medicare

- Legal separation of the covered employee and their spouse

- Bankruptcy

- Death of the protected employee

How Much Does COBRA Cost?

You must make monthly payments to keep your health plan after leaving your job. The average cost of COBRA health insurance premium is $400 to $700 monthly per head, and your employer will not contribute to this. However, you can opt for accident-only plans at $44 monthly or short-term medical payments from $80 monthly.

We recommend using the COBRA Premium Calculator to estimate your costs before proceeding with an application. If you miss your payments or don’t pay your premiums timely, the group health plan provider may issue an early termination before the scheduled end date.

How To Apply for COBRA Benefits

Once you meet the eligibility requirements above and have received a COBRA election notice from your employer or a COBRA administrator, follow the steps below to apply for the health benefits.

- Visit the COBRA application website and sign up.

- Access your account via the COBRA insurance login page and elect a plan within 60 days of receiving the election notice. You must complete and submit the COBRA election form online or hand it over to your administrator.

- Attach additional documents, such as proof of previous coverage and the qualifying event that triggered your need for COBRA.

- Make your first premium payment within 45 days and your insurance starts immediately. However, pay your monthly premiums when due to avoid termination.

The coverage duration is 18 to 36 months, but you can cancel or extend it under certain conditions. For an extension, the conditions include disability or the occurrence of a second qualifying event.

How Does COBRA Payment Affect Taxes?

Paying COBRA premiums can help reduce your medical expenses when filing taxes. If you highlight your deductions and your medical bills make up over 7.5% of your adjusted gross income (AGI) for the tax year, you’ll get a medical expense deduction.

How Does COBRA Interact With Other Health Insurance Options

Medicaid and the Affordable Care Act (ACA) are popular COBRA alternatives. You can apply for the low-cost insurance options if you wish to drop your COBRA coverage anytime or use COBRA for coverage while waiting for your application to the other programs to be approved.

However, while COBRA is funded at the federal level, Medicaid is at the state and federal levels, providing affordable healthcare to low-income households. As such, Medicaid is a cheaper option.

Similarly, the ACA is a lower-priced insurance option that subsidizes health insurance premiums through tax credits and cost-sharing initiatives. Moreover, while COBRA has a maximum 36-month timeline, ACA has no time limits, provided you continue meeting the eligibility requirements and paying your premiums.

Continued Employment Health Coverage with COBRA

With COBRA, you and your family can enjoy group health benefits for up to 36 months after losing your job or meeting other qualifying conditions. The program has a generous 60-day enrollment period that also makes it more accessible to applicants.

However, you’ll be fully responsible for the program’s premiums, not your current or previous employer. If you need help, you can speak with an administrator or healthcare insurance specialists. You can also call the COBRA helpline at 877-262-7241.

FAQ

1. Can I add family members to my COBRA plan?

Y ou can add one or more dependents, including a newborn or spouse to your plan. However, this comes at an extra cost per head. Notify your administrator about this, and they’ll guide you.

2. What can I do if my application for COBRA is rejected?

If your application is denied, check the notice for the reason. Usually, it’s a result of missing information or supporting documents. Speak to your administrator about it, fix the errors, and appeal the decision. Alternatively, you can opt for other health insurance coverage options, such as Medicaid and the Affordable Care Act (ACA).